Articles of Interest

Staying Ahead of Climate Risk: A Practical Framework for Protecting Real Estate NOI

Institutional investors typically accept that climate transition and physical risks are now variables which affect financial outcomes and should be actively managed. The question is how to manage them in a practical manner that supports informed decisions and enables investment and pricing conversations. This article walks through key investment insights from the past 20 years of real estate research and practice, then presents a broadly applicable climate framework for use by real estate investors.

For the past two years I have been working with Affine Climate Solutions supporting leading Financial Institutions in Canada. Through this work, I reviewed over 100 academic articles on the so called “green premium” in real estate. Researchers were looking to understand/prove whether investing in sustainability improved financial returns. Most of the reviewed research presented the analysis of large data sets from Europe, the U.S. and Asia. Financial performance of buildings was normalized for over 20 variables, such as size, location, asset class, age, Walk Score, etc. What remained constant is that assets without a green certification or improved energy efficiency experienced a Net Operating Income (NOI) erosion of 7–10% compared to equivalent greener buildings. This finding was similar across office and residential asset classes, and with some evidence for retail and warehouse. A further takeaway is that the evidence of the value difference is so strong that academics no longer study it – it is taken as proven.

During my time at Bentall Kennedy (now known as BentallGreenOak), we conducted one such study with two globally leading academics in the field. Two key findings were corroborated across many other studies: 1) The financial difference is the result of a combination of the following: higher tenant retention, lower tenant inducements, faster leasing velocity, and marginally higher face rents – all which lead to better net effective rents. 2) The delta of NOI erosion was twice as large in suburban office markets indicating that a lower supply of green buildings leads to higher value differences. Key lessons from the research and my experience during 2005-2024 are:

- Buildings ahead of the growing demand for green buildings performed 7%+ better.

- Energy efficiency investments frequently had IRRs of 30%+ from utility savings and delivered up to 40% efficiency improvements.

- Risk avoidance (NOI erosion in this case) was underpriced by the majority of the market and was rarely captured in valuations.

- Institutional buyers are pricing in green risk via changes in capitalization rates on transactions in leading markets such as NYC and London.

Energy efficiency and green certification were market disruptions. They were new criteria of quality which were organically priced in over time. Now, two additional concepts have been introduced: physical climate risk and carbon transition risk (net-zero/low carbon). Physical climate risk is changing as extreme weather events become more common and the chance that a building is damaged by flooding, wildfire or storm surge is increased. Carbon transition risk is the risk that carbon intensity regulations are passed, tenant start requesting or requiring low operational carbon buildings, and/or buyers have a similar preference or requirement. Together, they can be described as climate transition risks.

Real estate investment decisions typically include a sensitivity analysis that maps different capitalization rates against another variable such as NOI or net effective rent. Conducting a similar type of analysis is useful for better understanding climate transition risks given that capital costs of these retrofits are often higher than those from energy efficiency and they lack simple paybacks from utility savings. The outputs in this type of analysis are costs versus changes in future value. While there are robust service streams dedicated to planning and estimating climate transition costs, what has generally been lacking are useful frameworks for scenario planning of future value (at risk). I propose that they are best addressed by grouping them into four categories, as per below, and for each one creating low, medium and high scenarios.

A. Regulatory Risk

There were rarely clear regulatory risks linked to green certifications and energy efficiency in the North American market. However, these risks did emerge in the UK and some EU jurisdictions with growing minimum requirements around Energy Performance Certificates (EPCs). The research shows that the value difference is much greater when regulations come into play. The value difference jumps to 20% between buildings that meet the changing EPC regulations and those that do not.

To avoid both regulatory penalties and market pricing of non-compliance, research and scenario planning is required. With a strong majority of the global institutionally-investable real estate market in jurisdictions with stated 2050 net-zero targets, the question is more about when – than if – low carbon regulations will come into force.

With most operational carbon-heavy building equipment having lifetimes of 20-50 years, scenario planning gets easier. Installing electrified heating plants is typically a capital cost premium and, in many cases, has a marginal utility payback over its lifetime (or worse). The regulatory risk question is then: What is the percentage chance that regulation will come into force during the lifetime of that piece of equipment? Using low, medium and high scenarios, an estimate of the net-zero capital that would need to be spent can be evaluated (on top of any non-net-zero capital replacements done in the meantime).

B. Leasing Risk

Building or retrofitting to a standard like LEED is relatively inexpensive and can be done relatively quickly with an experienced team. If tenant demand shifts in the leasing market to certification being a preference or a requirement, it can usually be achieved within a year or two. On the other hand, retrofitting a building to net-zero or re-designing a new building midway through, takes longer and is much more capital intensive.

If the market shifts, as we are seeing initial evidence of in London and other global cities, an owner or asset manager’s ability to react is much harder and could take 5-10+ years. Modelling the downside risk of not meeting market expectations for net-zero/low carbon buildings is challenging given the lack of available data.

It is reasonable to expect that markets will react to net-zero/low carbon much like they did to green certification and energy efficiency. If so, buildings that are not aligned will face lower tenant retention, longer rent-free periods, increased tenant inducements, and slower lease-up velocity. Low, medium and high scenarios that consider the extent of market/leasing preferences and a starting date for those preferences can support with financial risk modelling.

C. Physical Risk

The academic research on physical climate events and relative physical climate risk exposure to acute events (predominately flooding, coastal surge, and wildfires) generally shows that valuation impacts are small and disappear 6 months to 2 years after a major event. Through my research, I have not found a study showing a pricing impact of a building’s readiness to long-term impacts such as heat stress or drought.

On the positive side, there are many data providers that can provide annual probable loss calculations given a building’s location. The concern for investors is that property insurance re-prices annually and in severe cases, may no longer be available.

The financial impacts are fourfold: 1) Annual likelihood of acute climate event, 2) Annual likelihood of damage costs, 3) Rapidly increasing insurance costs, and 4) Uncertain capital costs for readiness. Working with a leading data provider can give reasonable financial estimates. The Australian market is a leader in these analyses and show it can be done.

D. Exit (Valuation) Risk

While some climate transition risks may appear in building values through the factors above, they may significantly under-represent the risk weightings placed on these buildings by investors who are looking ahead to the next ten years. Based on evidence from LEED and BREEAM-certified buildings, this can take the form of changes in exit capitalization rates often in the 20-40 basis point range. Even better, in my experience, I have seen two comparable offices sold in London, UK for a 250+ basis point spread with one of the greatest differentiators between the buildings being net-zero and BREAAM performance.

Scenario Planning Framework

Taking the above four risk categories into consideration, the following three future scenarios provide a useful framework for value at risk planning:

Low Risk: The future looks much like the present with slow regulatory advancement, minor tenant demand, and limited physical disruption.

Medium Risk: The future of climate transition roughly follows the path of green certification and energy efficiency. Regulations advance in a patchwork, tenant demand grows but is varied by sector and asset type, insurance costs surge, and physical damage increases.

High Risk: Decarbonization policy advances rapidly in the next government cycle, tenants demand quality buildings with low carbon footprints, and acute climate events affect whole markets (cities/regions).

For each of the four risks, a financial value for each scenario can be created through a combination of historical precent research, as well as regional and asset class data.

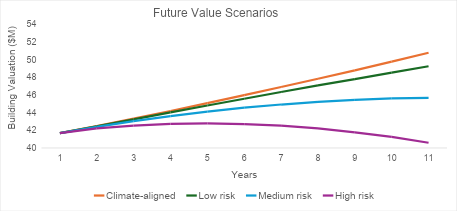

For example, the graph below illustrates how building value evolves over time under the three future scenarios compared to a building that undergoes a climate transition-aligned retrofit. In this example, a 100,000 square foot office building undergoes a $3 million net-zero retrofit, which does not generate simple payback through utility savings but preserves and enhances long-term value. The low, medium, and high-risk scenarios represent increasing levels of value erosion associated with doing nothing, based on assumptions informed by research, regional conditions, and asset class data. As shown, while the climate-aligned path steadily increases value (CPI average for simplicity), the three scenarios diverge over time, with higher risk assumptions leading to more significant value loss. The graph demonstrates that the cost of inaction can exceed the upfront retrofit cost, depending on how transition risks materialize.

.png)

How does this lead to better decision making?

The pressing question facing investors around the climate transition is: What is the downside risk (value at risk) of doing nothing versus retrofitting to be ready? Based on precedent from research on energy efficiency and green certification, the answer is somewhere between 3-20%. Then the questions are: How much will it cost to retrofit the asset? And what is the optimal retrofit timeline based on the age of the building components and equipment? Once that is determined, the next question is whether to approve the retrofit capital plan or to sell the asset before the majority of the market knows how to price it.

In previous roles, I advised the sale of over $2 billion of assets with acute physical climate exposure at a time when the buyers did not factor in the climate risk to the purchase price. A similar pattern is emerging around selling assets where the cost of retrofitting to net-zero is higher than the medium or even high scenarios outlined above. To be prepared, now is the time for investors, owners and asset managers to better understand these risks and the costs, even if it is not deemed a good time in the market cycle to spend money on a retrofit.

In closing, markets and valuators have rarely fully priced climate transition risk into building valuations. Investors who act early on retrofitting the right buildings will preserve income and protect asset value. Those who delay will not just miss any possible upside, they will likely see a further NOI and exit value drop of 7-10% based on the precedent set in the last sustainability cycle of green certifications and energy efficiency.

Jamie Gray-Donald, PhD, Founder, Recursive Advisors

Jamie Gray-Donald, PhD was an academic who pivoted to being a corporate sustainability leader for 16 years, first in retail then in real estate. He built industry-leading strategies, led high-performing teams, and delivered profitable results within large, complex organizations. He has a track record of enhancing portfolio value through investing in decarbonization planning, transition finance pathways, and implementing scalable, cost-effect standards that optimize businesses and assets. Jamie successfully delivered profitable strategies at scale, including the creation – from scratch – of a globally recognized ESG platform for a $94 Billion investment portfolio. Jamie founded Recursive Advisors in 2025 and is now supporting a dozen clients with a main focus on managing climate risks of financial institutions and real estate companies. Jamie is also a Senior Advisor to Affine Climate Solutions and the father of three young daughters who have been promised that climate change will be resolved before Jamie retires.