Articles of Interest

Protecting Beneficiary Outcomes in a Complex World

.jpg)

The term systemic risk was coined by William Cline, an economist during the early 80’s Latin American debt crisis1. He used it to describe a scenario whereby defaults by major debtor countries could trigger a collapse of the international financial system.

The UK Institute & Faculty of Actuaries concluded that humanity is now facing an increasing risk of “Planetary Insolvency” — a level of systemic breakdown where critical ecosystem services (food, water, regulation of the climate) can no longer reliably support society and the global economy2.

The goal of this article is to educate on climate systemic risk and to present a case study about a plan sponsor that uses real-world analytics and narrative to help make strategic decisions, as part of their fiduciary duty, to protect beneficiary outcomes near and long term.

The State of Climate in 2026

Up to now, climate change has been linear and gradual. We are now entering a zone of potentially highly non-linear shocks, which will cascade into food, water, energy, financial and social system disruption.

For example, as of today, 50% of the United States and Puerto Rico and 60% of the Lower 48 states are in drought3. Overlaying that with disruptions to fertilizer and oil price shocks, gives a concerning prospect of breadbasket shocks, food price inflation and significant societal challenge emerging later in 2026 and through 2027.

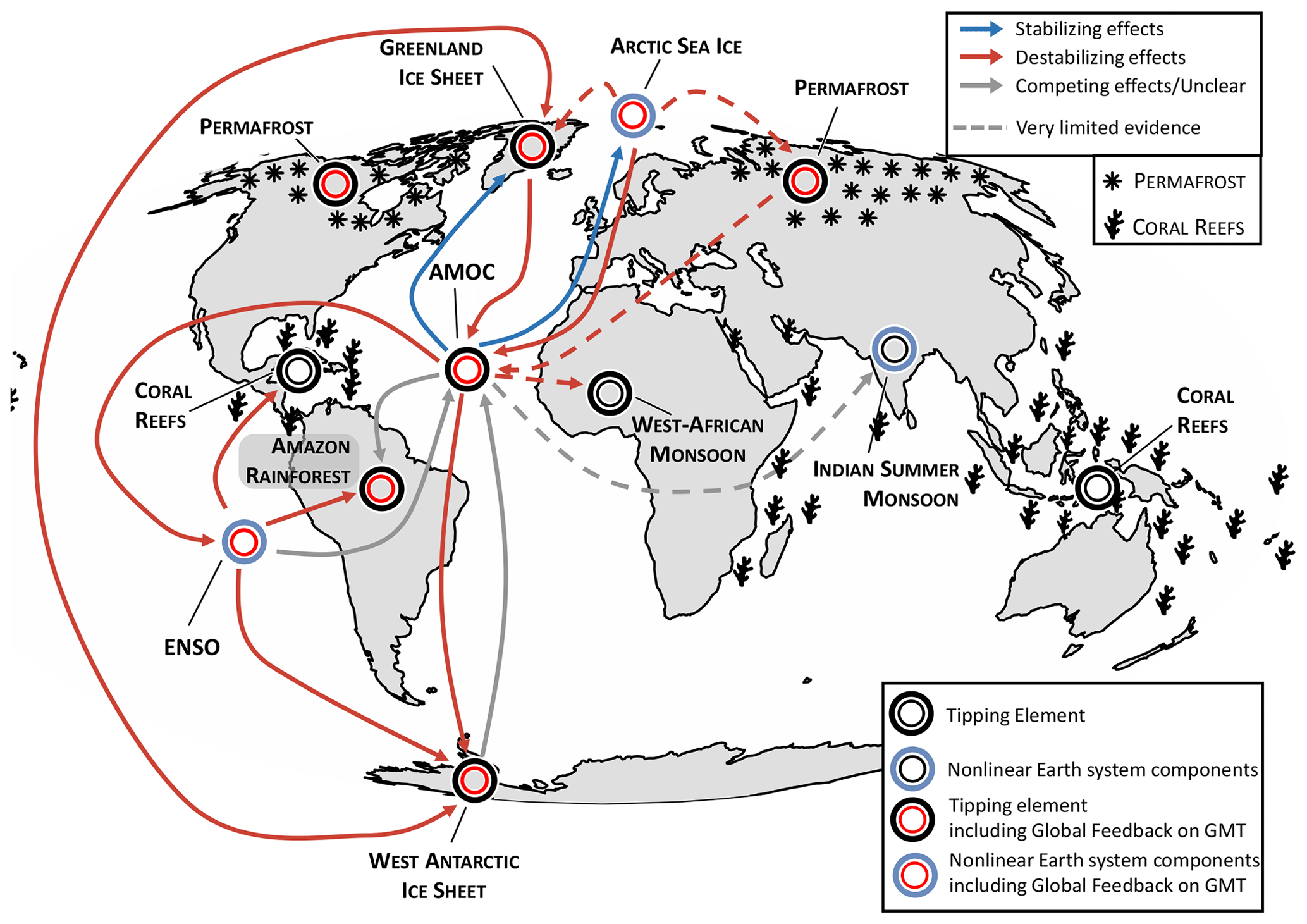

A tipping point is a critical threshold in the Earth system which, once crossed, can trigger large often irreversible changes in the climate. Warm‑water coral reefs, crucial to a billion people and almost a million species, are experiencing unprecedented mortality. The chart below shows other tipping points that are moving into a danger zone.

https://esd.copernicus.org/articles/15/41/2024/

Scientists are observing that the planet is warming more quickly than expected and is more sensitive to greenhouse gases than we assumed when we set carbon budgets5.

On the positive side, according to the IEA6, renewable energy deployment is hitting record highs, with solar and wind dominating new capacity additions. Battery storage investment is expanding rapidly, and EV adoption continues to accelerate across major markets, although coal use remains stubbornly high.

Let’s be clear, although the transition to net-zero will go on, it now looks unlikely that it will prevent global temperatures from exceeding the Paris Goals, increasing the level of physical risk disruption we will face.

Two risk lenses pension plan fiduciaries can adopt

Pension plan administrators have a fiduciary duty to manage assets in the best interest of their beneficiaries (both current and future). Canadian Pension Regulators (CAPSA) clearly puts the onus on pension plan administrators to determine the materiality of climate risk7.

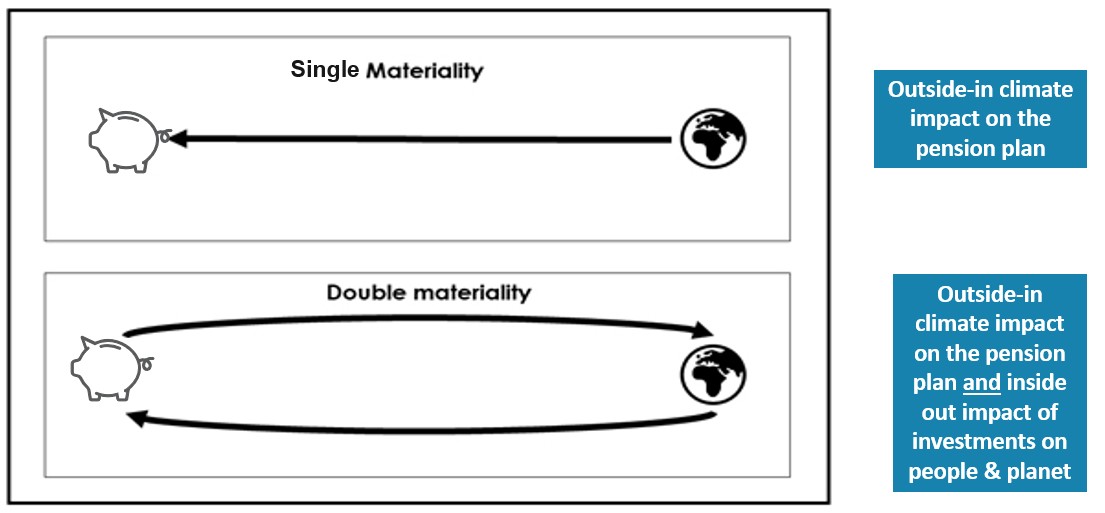

There are two levels of materiality to consider:

a) Single materiality: refers to the impact of climate change on the risk and return profile of a pension plan ( the outside-in climate impact)

b) Double materiality: considers both single materiality and the inside out impact of investments on people and planet. Fiduciaries who adopt this lens are part of the global pool of capital allocators who collectively finance the transition to net-zero to minimize the systemic risk of climate change on future beneficiaries.

Seven of the eleven largest Canadian pension plans have adopted a double materiality lens and have committed to net-zero emissions by 2050 or sooner in line with the Paris Agreement 8.

Issues with first generation climate scenario analysis

First generation climate scenario analysis produced benign physical risk results in high warming scenarios and ignored systemic risks. This was counterintuitive and at odds with climate scientists’ views that climate change could redraw the map of human survival9.

The limitations of these first-generation approaches have been extensively documented by academic, actuaries and industry organisations10. These include:

- over-reliance on linear modelling of global temperatures

- ignoring tipping points geopolitical conflict, migration and more

- unrealistic assumption of ongoing economic growth, regardless of the scenario modelled

While these models may provide some reassurance that “the future ain’t so bad,” they are at odds with both climate science and sound risk management principles.

The response to first generation shortcomings

The need for more realistic and real-world climate scenarios, which include non-linear climate and societal responses, has been recognised. Several groups developed outputs and guidance. One of the most influential global financial institution, J.P. Morgan, is starting to connect the dots11.

In the UK, the Bank of England recently published guidance12 that highlighted the limitations of climate change scenario analysis and the need for regulated firms to consider these. Papers have been published by academics and leading pension schemes on ways to develop more realistic and real-world narrative scenarios13. The UK Pensions Regulator has also acknowledged industry concerns about the limitations of current models”14.

Case study: Brunel Pension Partnership

Brunel Pension Partnership is a UK Local Government Pension Scheme pool managing assets for ten partner funds (£36B or $67B in AUM). The company faces similar expectations as Canadian plans—most notably on climate change—alongside mounting scrutiny of how Pension Plans address nature-related financial risks.

At the core of Brunel’s approach is a conviction that long-term financial performance depends on the stability of the natural and social systems underpinning economic activity. This maps closely onto the planetary boundaries’ framework15, and rather than treating these boundaries as constraints, Brunel embeds them as financially material risk factors relevant to any investor with a multi-decade horizon.

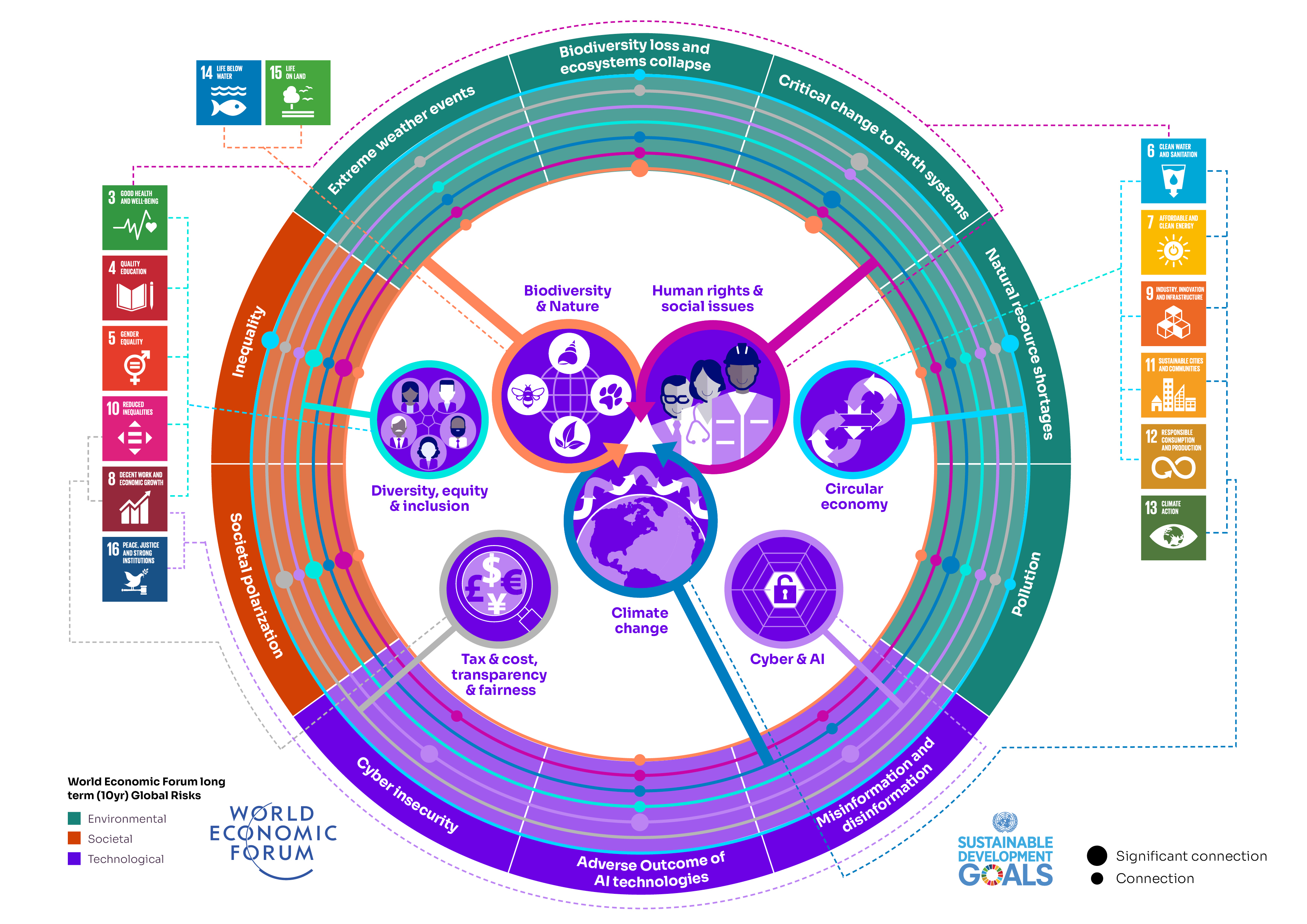

Brunel sets its Responsible Investment (RI) priorities through a double materiality lens. This is informed with reference to emerging science (e.g. planetary boundaries), the UN Sustainable Development Goals and by using World Economic Forum global risks to identify interconnections and sense-check priorities.

This has resulted in three top-level RI themes — Climate Change; Biodiversity & Nature; and Human Rights & Social Issues — spanning several of the most critical planetary boundaries, from atmospheric stability to biosphere integrity. The 2026 mapping of Brunel’s strategy is illustrated below.

The mapping to risk, opportunities and interconnections helps formulate an action plan looking at the different levers that can be used by pension funds from:

- integration into risk management,

- capital allocation (particularly seeking positive opportunities), and

- collective and individual stewardship and engagement activities.

On climate, Brunel’s Climate Change Policy 2023–2030 outlines a comprehensive set of actions focused on the required system-level changes, not just portfolio adjustment. For example, they committed to:

- changing the rules of the financial system by demanding that Net Zero and resilience be turned into clear, enforceable policy plans

- advocating for meaningful carbon pricing and the removal of perverse subsidies

- Expecting investment managers to be able to demonstrate controversial holdings are aligned and escalate engagement

- driving the development of Paris-aligned products across all asset classes.

On nature, Brunel has committed to adopting the TNFD framework and is one of the early adopters and has analysed deforestation and water exposure risks of its listed equity portfolios.

Brunel also invests directly in natural capital solutions. Its Cycle 3 Infrastructure portfolio includes the Meadow Lark Lands Fund, focused on organic farmland aimed at improving soil health, sequestering carbon, reducing pesticide runoff, and delivering biodiversity and ecosystem co-benefits.

Critically, Brunel acknowledges that many of these systemic risks sit outside traditional financial analysis but are financially material when properly assessed — and that failure to price them correctly can lead to portfolio underperformance against benchmarks that simply mirror that mispricing. For a long-term investor serving pension beneficiaries, accepting benchmark-relative underperformance in the short term to avoid systemic risk in the long term is not a values trade-off — it is fiduciary duty properly understood.

Conclusion

“The task is large, the window of opportunity is short, and the stakes are existential16” is how our Prime Minister Mark Carney characterised the global efforts needed to avoid the catastrophic impacts of climate change. Pension plan fiduciaries have agency, they can develop an action plan to position their portfolio, as well as engaging with policy makers/governments to help avoid this worst-case scenario. The tools are emerging now to help them do so. It just takes knowledge, conviction, and action, both individually and collectively.

1The Emergence of Systemic Financial Risk

2Planetary Solvency – finding our balance with nature

4Global Tipping Points | understanding risks & their potential impact

6Renewables 2025 – Analysis - IEA

7CAPSA Guideline No 10 for Risk Management for Plan Administrators

8Emissions Reduction Targets – Report Card 2025 — Shift - Protect Your Pension and the Planet

9Planetary Solvency – finding our balance with nature Global risk management for human prosperity

10See for example: ACPM | ACARR - Climate Scenario Analysis: From Information To Emotion To Conviction, https://greenfuturessolutions.com/news/recalibrating-climate-risk/, https://www.fca.org.uk/publication/corporate/developing-approach-nature-risk-financial-services.pdf, The Emperor’s New Climate Scenarios Limitations and assumptions of commonly used climate-change scenarios in financial services

11J.P. Morgan Is Thinking About Climate Tipping Points

12SS5/25 – Enhancing banks’ and insurers’ approaches to managing climate-related risks

13USS and University of Exeter No Time To Lose New Scenario Narratives for Action on Climate Change

14TPR calls on trustees to make climate scenario analysis ‘useful’ amid criticism | News | IPE

André Choquet, FCIA, FSA, CIM

President & Founder, Mathalian Partners

André is an actuary and an investment professional with over 30 years of experience advising pension plan sponsors on governance, design, funding, and investing. For the past 10 years, he has helped integrate sustainability risks and opportunities into investment processes.

André founded his Toronto-based firm to help asset owners develop and implement climate strategies. In 2025, he was appointed to the UK Institute and Faculty of Actuaries Planetary Solvency Task Force to lead outreach efforts aimed at asset owners, policy makers, politicians, and financial sector executives.

André received the 2022 Canadian Institute of Actuaries President Award for his role as Chair of the CIA Climate Change and Sustainability Committee (2021-22) and his dedication in progressing the integration of climate change in the practice of the Institute’s 6,000 members. He is an experienced speaker and author on a variety of pension topics and contemplative practices.

Sandy Trust, IFOA

IFOA Planetary Solvency lead

Sandy is the Past-Chair of the UK Institute and Faculty of Actuaries Sustainability Board. He is the lead author of a series of collaborative research reports which bring together science and risk, seeking to improve policymaker level risk management. The latest report Planetary Solvency – finding our balance with nature, explores how actuarial techniques can help society manage climate change and other risks. This builds on the findings from Climate Scorpion – the sting is in the tail – which highlighted concerns around carbon budgets being unrealistic and The Emperor’s New Climate Scenarios – which highlighted the limitations of commonly used climate scenarios.

Sandy’s personal mission is to help re-connect finance and the economy to nature and the biosphere to deliver a future worth living in, he works with investors and advises several regulator and policymaker groups on these topics.

Faith Ward, MBE

Chief Responsible Investment Officer, Brunel Pension Partnership

Faith has nearly three decades of experience advocating for systemic risk awareness in finance and investment. Most recently Chief Responsible Investment Officer at Brunel Pension Partnership and Chair of the Institutional Investors Group on Climate Change (IIGCC), she has helped shape policy and design investment solutions that deliver long-term value for asset owners and beneficiaries.

She chairs the Working Group for Scaling Finance at the Transition Finance Council, focusing on hard-to-abate sectors, and is an Ambassador for the Transition Pathway Initiative, which she co-founded. Her advisory roles include the Church of England's Ethics Investment Advisory Group, the ISSB Investor Advisory Group, and the ATTENUATE adaptation project from the London School of Economics Grantham Research Institute. She is also a Climate Ambassador for the National Federation of Women's Institutes.

In 2025 Faith was awarded an MBE for services to pensions and the environment. She is a Fellow of the CFA (UK).