Articles of Interest

Navigating conflicting ESG ratings

Increasingly, pension fund managers are seeking to incorporate environmental, social, and governance (ESG) data into their already rigorous financial analysis when researching companies as potential investments for their portfolios. At first glance, the process would seem straightforward – contract with a rating agency to furnish a reliable ESG analysis of the company in question, which is then distilled into an “ESG rating score.” Depending on the managers’ overall investment criteria, a higher or lower ESG rating will not necessarily, of itself, qualify or disqualify a candidate from investment. But it can tilt the managers’ risk weighting one way or the other.

However, ESG ratings have recently come under more scrutiny. ESG ratings can vary significantly from agency to agency, sometimes leaving managers at a loss as to which rating to accept. Critics cite lack of consistency and lack of transparency among rating agencies as the main causes of concern.

This alone is not a sufficient reason to reject ESG ratings altogether. ESG ratings provide a quantitative, relatively unbiased, means for comparison. The reality is that there are some real benefits to ESG ratings, but there are also some significant drawbacks. Here’s a look at some of the deficiencies and some of the benefits in ESG ratings.

Deficiencies

We will start with some of the commonly stated deficiencies of ESG ratings, the first one being a lack of consistency. By this we mean that the scores can vary from one rating provider to another. This, of course, depends on different methodologies and how you’re looking at the data.

Some ratings providers show a rating based on the industry or sector of the company. So, for example, oil companies would be ranked only against oil companies. Others will show the universal ranking, where industry and sector doesn’t matter, so an oil company could be ranked against a tech company.

The solution to this anomaly is to move away from comparisons by sector. In the age of the climate crisis, oil and gas companies should not be getting better scores than solar companies.

The ESMA Report on Trends, Risks and Vulnerabilities No. 1, 2021 states that a study done on the ratings from five prominent data providers shows 60% correlation across ESG ratings. This naturally results in different index construction and different holdings for funds and ETFs tracking those indexes. Let’s take three ESG index-tracking ETFs as an example (see Table 1).

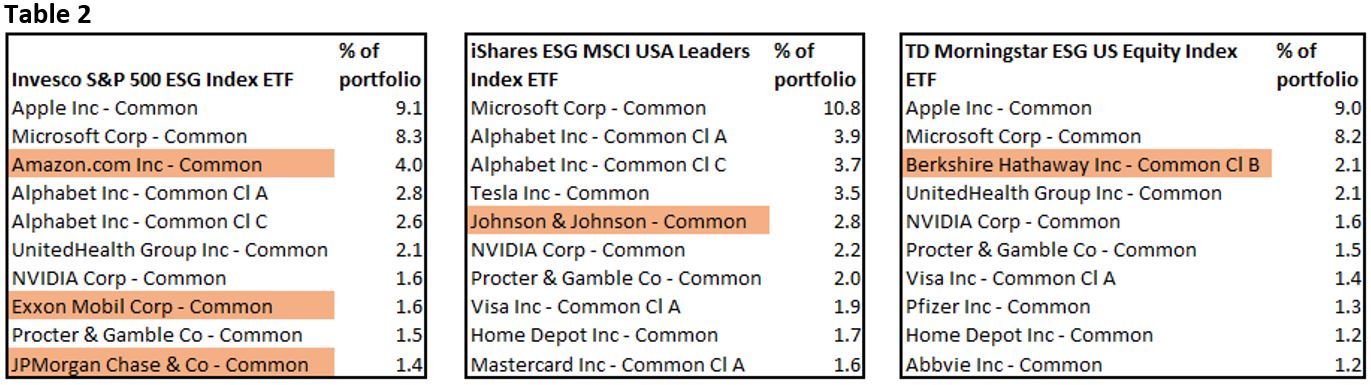

The underlying indexes are from S&P, MSCI, and Morningstar/Sustainalytics, and all are focused on the U.S. market with ESG filters. Table 2 shows a snapshot of the top 10 holdings for each fund.

There is a lot of overlap in holdings, but there are also a few crucial differences. The companies highlighted in Table 2 do not belong to either of the other two funds. The one that really jumps out is Exxon Mobil in the S&P list. The key here is that the S&P 500 ESG Index targets 75% of the float market capitalization from each GICS industry group. In other words, there are many companies from the energy industry in the S&P ESG Index. S&P publishes a list of exclusions, which consists of any company with an ESG score in the bottom 25% of their industry group.

The MSCI index also targets companies with high ESG ratings in each sector and, like the S&P index, has a list of exclusions. One key exclusion is that any company with an MSCI ESG Controversies Score below 3 is not eligible. The Sustainalytics Index has a similar exclusion based on controversies, which might be why Exxon Mobil does not show up in their indexes.

This leads to one of the other deficiencies in ESG ratings: the lack of transparency.

Ultimately, we don’t know exactly why Exxon is excluded from the MSCI and Sustainalytics indexes. In general, it’s usually easy to see how a company scored on each of the metrics, but it’s very hard to see the company-specific data that led to that score.

But, as an analogy, we don’t really know exactly why a company gets assigned to a certain sector either. Different data providers have different methodologies for sector classifications, and sector allocations are widely accepted.

Benefits

With ESG scores what we do get is very good methodology documents. In fact, these are provided in detail to the point where you can see all the factors that are being measured. And the fact that there are differences in the scores is not necessarily a bad thing. ESG investing means different things to different managers, so the fact that we have a choice and can pick a methodology that aligns with our values should be seen as a positive.

The best attribute of ESG ratings is that they provide a simplified means for comparison. Without them, there is no way we could compare thousands of companies across the same metrics. The ratings are probably our best defense against greenwashing. Otherwise, we are left to read the lengthy reporting on climate solutions done by individual companies themselves, hardly an objective assessment.

Or you could look at the ESG scores that measure real results and see how they compare with peers in their industry or against a global universe. Sustainalytics4 has Exxon rated as “High Risk” and ranks it in the top 25th percentile in their industry group (oil and gas producers), but it drops to the 83rd percentile when compared with the global universe that disregards industry. MSCI shows Exxon as “Average” in the integrated oil and gas industry, but states that it is “strongly misaligned with global climate goals” and says it is not an ESG Leader “on any of the Key Issues” evaluated for the industry.

Given the variety of ESG ratings methodologies used by various ratings agencies, the best approach for managers is to drill down into the processes and settle for one that most closely aligns with their investing values. Alternatively, managers might consider all the ESG ratings available for a particular investment candidate, and use a consensus rating. A company like OWL ESG, for instance, uses the “wisdom of the crowd” approach, gathering data from over 500 sources, including the majority of the major ESG research firms. This results in ESG scores that reflect the consensus on a company.

Ultimately, ESG ratings are not perfect and naturally should not be the only consideration when looking at a company or a fund through an ESG lens. But they can be a valuable and necessary part of the overall research process.

Reid Baker, Vice President, Analytics and Data, Fundata Canada Inc.

Reid Baker is Vice President, Analytics and Data, at Fundata Canada Inc. He is involved with research and development of quantitative measures and models to analyze investment fund products, including Fundata Prospectus Risk Indices, the Fundata ESG Ratings, and the FundGrade A+ RI award. Reid has been in the financial data and analytics industry for 14 years and Chaired the Canadian Investment Funds Standards Committee (CIFSC) for nine years. He holds the Chartered Enterprise Risk Actuary (CERA) credential, as well as the Associate of the Society of Actuaries (ASA) designation.