Articles of Interest

ESG Integration Challenges & Opportunities For Pension Plans

As investment consultants, we've observed how Environmental, Social and Governance (ESG) considerations are becoming increasingly important factors in the management of pension plan assets and fiduciary obligations. Additional forces adding to the accelerated interest in ESG adoption are the speed at which regulatory changes are being made locally and globally, and a push by plan members to align their pension investment outcomes with sustainability.

This shift has presented both challenges and opportunities for all institutional investors however, for pension plans in particular, trying to balance competing interests between fiduciary obligations, while responding to the interests of various stakeholders, ESG integration can seem overwhelming to achieve at best and at worst, implemented haphazardly opens up potential risk and liability for trustees. In this article, we highlight some important considerations and best practices for pension plans integrating ESG.

Concepts that underpin any approach

In every decision or approach to integrate ESG, fiduciary duty and the primary purpose of the plan serve to underpin the investment decisions made for the plan. Enough has been written about the fact that ESG considerations are indeed relevant if they are financially material to the long-term performance of the plan. However, not enough is said about the fact that fiduciary duty is evolutionary – it evolves and changes with our growing body of knowledge and societal norms. In the research paper “The Public Fiduciary: Emerging Themes in Canadian Fiduciary Law for Pension Trustees” Waitzer and Sarro make the point that “fiduciary law is not static, nor, in the context of trusts, is it tied to a particular investment theory. It has proven to be a remarkably flexible set of principles, subject to varying interpretations over time”. In the context of ESG integration, as our understanding of how such issues impact investment performance, and as stakeholder expectations evolve, so too will expectations of fiduciary duty evolve and may be reinterpreted. Therefore, irrespective of plan type, size or implementation approach, ESG investment thesis will need to be adaptive and governance practices reviewed regularly.

Having a roadmap

ESG integration is more than making investment decisions and selecting managers. It is a process with interdependent steps that should address each component of plan management so that ESG integration will ‘hang together’. When we work with clients to integrate ESG we found the use of a documented responsible investment framework helpful. It’s like a roadmap that identifies the key steps and decisions that will need to be taken by trustees. Not only will it simplify the implementation process but it will also ensure it is done holistically, e.g. the investment beliefs, investment decisions and expected outcomes are all aligned and bring clarity to how desired outcomes will be achieved.

Practical considerations

A common issue we see in many statement of investment policies and procedures (SIPP) is a disconnect between the ESG investment policy and the investment approach taken. For example, specified investment limits, targets, and proxy voting statements may not be implementable because the plan holds pooled funds, and those decisions are made by managers. While fund unitholders may exercise voting rights over certain aspects of the fund, how much risk to take and security selection decisions are made by the manager. When developing an ESG policy, trustees need to consider which decisions are within their control and can be reasonably achieved, if the investments will be pooled or unitized investments. For example, ESG policy can focus on selecting managers with strong ESG processes, choosing fund strategies aligned with ESG goals, and requesting information on managers' proxy voting policies and practices related to ESG issues. Trustees can also engage in stewardship activities by joining organizations that advocate for change and better disclosure and transparency by companies, e.g., CDP (Carbon Disclosure Project), the UN PRI, Climate Action 100+ etc.

Using ESG Metrics and Third-Party Data

Identifying greenwashing is a growing concern as sustainable strategies gain momentum. The volume of ESG data and lack of standardization make it challenging to identify greenwashing and validate the accuracy of a manager or a company’s ESG initiatives. Being able to compare two managers with similar fund strategies – both of which may be UNPRI signatories, is critical not just to identify potential greenwashing, but also identify how the funds in the portfolio align with the ESG policy of the plan. Managers employ diverse methods to integrate ESG into the investment decisions for their funds and third-party data providers use different methodologies when rating ESG factors. Adding a qualitative due diligence process seeks to evaluate investment managers’ ESG process by looking ‘under the hood’ using a consistent and standardized approach. The use of ESG metrics from third-party data providers can then be used to enhance qualitative assessments and identify potential greenwashing allowing for better apples to apples comparability and a more robust manager assessment.

Monitoring and Reporting

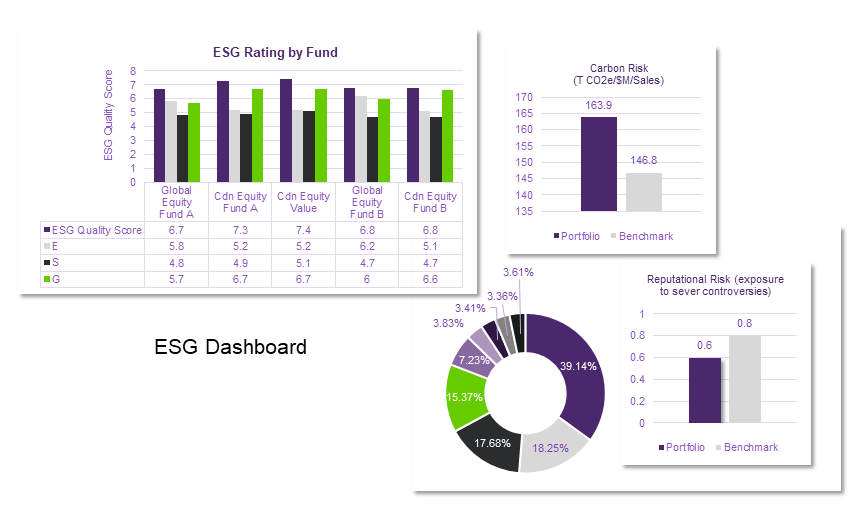

Reporting on ESG metrics is essential once ESG is integrated into the plan. It demonstrates the alignment of actions with words and enables trustees to effectively communicate their commitment to ESG principles and meet governance obligations. Including an ESG dashboard or targeted reporting that provides quantitative ESG data, such as carbon intensity and GHG emissions, combined with qualitative analysis of managers' ESG processes, helps trustees make informed decisions and measure progress towards sustainability goals while evidencing governance actions to stakeholders.

Use of Reporting Frameworks

The Taskforce on Climate-related Financial Disclosures (TCFD) developed by the Financial Stability Board (FSB) in 2017 as a disclosure standard for systemically important financial institutions and public companies has largely been adopted by pension plans globally as the accepted framework to assess, manage and monitor the impact of climate-related risks and opportunities on their pension plans. The TCFD framework was one of several disclosure frameworks in existence (others include SASB, GRI standards, CDP etc.). During COP28 as part of the push to standardize and develop a baseline reporting framework it was agreed that the International Sustainability Standards Board (ISSB) would take-over TCFD. The ISSB builds on the TCFD and SASB standards. To ensure Canadian interests are reflected in the standards, the Canadian Sustainability Standards Board (CSSB) was created in June 2023. The CSSB will work in lockstep with the ISSB to develop standards reflecting Canadian-specific modifications. The proposed disclosure standards (CSDS 1 and 2) will be available for public comment in March and June 2024. On June 28, 2023, eleven of Canda’s leading pension plan investment managers who report using the TCFD framework, e.g. CPP Investments, AIMco, HOOPP, BCI, Caisse de dépôt et placement du Québec, etc. support the transfer to ISSB and the new IFRS reporting framework. Regulatory bodies like the CSA and OSFI have also stated they will look to align with the new ISSB standards from TCFD.

Gap analysis

With all this in mind, it is important to take inventory of the required resources, capacity, and current knowledge level of trustees. Third-party expertise can include actuaries and investment consultants to help with climate scenario analysis and developing ESG policy, legal counsel to help understand fiduciary duty, and investment managers to understand ESG risks and opportunities. By leveraging third-party expertise, trustees can effectively fill knowledge gaps and ensure a comprehensive and informed approach to ESG integration.

Taking into account these important considerations and best practices, pension plans can effectively integrate ESG and navigate the challenges and opportunities it presents.

Alana Dubinski, CIM, Chief Compliance Officer for TELUS Health Investment Management

Alana Dubinski is Chief Compliance Officer for TELUS Health Investment Management and heads up ESG strategy and programs for TELUS Health Consulting clients. Alana brings over 25 years of investment industry experience developing and overseeing compliance programs and managing operations for financial institutions, consulting organizations and wealth management firms. At TELUS Health, Alana provides strategic direction, support and contributes to thought leadership in the areas of ESG integration and governance consulting across all facets of investment consulting services offered to clients.