Articles of Interest

Shaping Retirement Outcomes: How Boards and Plan Sponsors Can Navigate the Gender Pension Gap

Every year on March 8th, we mark International Women’s Day by celebrating the accomplishments of female leaders and highlighting the progress made toward gender equity. By the end of the month, however, we are reminded of just how much further there is to go. This year, March 26th marked Equal Pay Day; the date that represents how far into the new year women must work to earn what men, on average, were paid in the previous year.

This wage gap has clear and immediate implications for everyday affordability. It also has a longer‑term effect: it limits the ability to save for key life events such as home ownership and ultimately retirement, contributing to a persistent gender pension gap.

More than an equity concern, the gender pension gap is an identifiable, measurable risk with workforce and financial implications over a long-time horizon.

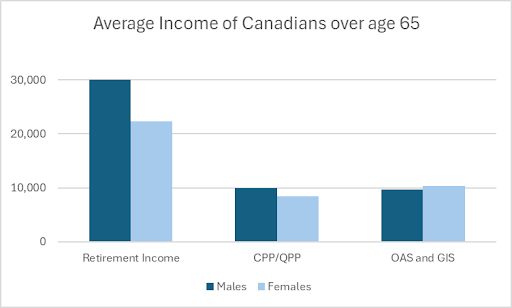

Statistics Canada data on retirement income by gender1 show roughly a 25% gap in non-government retirement income. In contrast, Old Age Security (OAS) and Guaranteed Income Supplement (GIS) income is slightly higher for women than for men, suggesting a higher GIS income for women and aligning with the greater prevalence of low income among older women (about 20%) compared with older men (about 14%)2. The gender pension gap is rooted in several interrelated factors: a well-documented gender pay gap, structural labour-market patterns such as women’s greater likelihood of career breaks and part-time work, and the continued under-representation of women in leadership roles, where they hold under 30% of executive positions in Canada3.

Once we account for earnings patterns, contribution capacity and career trajectories, many women arrive at retirement with lower income than their male counterparts. The gender pension gap presents both a future financial issue for women and a set of current risk considerations for plan sponsors and boards.

The Gender Pension Gap Through a Risk Management Lens

The gender pension gap gives rise to a range of interconnected risks for employers that extend well beyond retirement itself. From a workforce perspective, inadequate retirement savings among women can contribute to delayed retirements, succession bottlenecks and reduced flexibility to reshape the workforce over time, creating workforce and succession risk.

It can also influence employer brand and talent outcomes. As employees increasingly expect equitable total rewards, visible gaps in retirement outcomes may gradually erode trust and engagement and affect an organization’s ability to attract and retain female talent, with corresponding reputational and ESG risk as stakeholders focus more closely on equitable outcomes.

Longer‑term financial risks may arise as misaligned retirement patterns and undersaving can add strain on benefit and compensation budgets or limiting an organization’s ability to adjust its workforce cost base in line with strategy. Productivity and wellbeing are part of the picture as well, financially stressed employees have been shown to lose more than eight hours of productivity per week4, and the National Payroll Institute estimates that financial stress translates to $69.5 billion in lost productivity each year in Canada.

These effects tend to build gradually. The gender pension gap is therefore best viewed as a long-horizon risk: foreseeable, quantifiable and shaped by today’s plan design and workforce decisions, with impacts that may only become fully visible many years down the road.

For boards, pension committees and total rewards leaders, this also introduces governance and fiduciary oversight risk, as they are increasingly called upon to have visibility into how retirement programs are functioning for different segments of the workforce and to ensure that outcomes remain aligned with the organization’s overall risk, DEI and ESG priorities. Many organizations are taking a closer look at how those priorities show up in day‑to‑day practices and longer‑term outcomes. Understanding how retirement plans and practices interact with gender is a growing part of that conversation .

Getting Started: Practical First Steps

Boards and pension committees that wish to better understand and address the gender pension gap may find it helpful to take a phased, practical approach, focusing first on clarity of objectives, governance, data, design, and communication.

1. Set clear objectives and successful measures

Clarifying goals and guiding principles is an important foundation for any gender pension gap strategy. Clear, shared objectives make it easier to prioritize actions and to track progress over time.

- Consider what “closing the gap” could mean in your context. For example, reducing projected retirement income gaps, improving coverage levels, or increasing retirement readiness scores by gender.

- Align these objectives with broader DEI, total rewards and workforce planning priorities.

2. Establish a governance framework and dashboard

A robust governance framework helps ensure that gender‑related retirement outcomes are monitored and discussed on a regular basis. Highlighting a set of clear metrics can help turn complex information into insights that decision‑makers can act on.

- Agree on a set of gender-aware metrics (e.g., participation, contribution rates, account balances or accrued benefits, projected incomes) that can be tracked over time.

- Summarize key metrics, actions and milestones in a dashboard.

- Integrate gender pension gap indicators into existing board, pension committee, and total rewards reporting.

3. Leverage data and analytics

Thoughtful use of data allows sponsors to move from assumptions to evidence. Understanding where gaps emerge within your own plans and workforce can help focus effort where it will matter most.

- Analyze participation, contributions, accruals and projected retirement incomes by gender, age, pay bands and employment type.

- Look for patterns that may indicate where women are more likely to fall behind. For example, after parental leave, during part-time periods, or at particular career stages.

4. Identify barriers in plan design and practice

Plan design can unintentionally reinforce underlying labour-market patterns. Periodic reviews with a gender lens can help identify features that may be creating and/or underpinning barriers to equitable retirement outcomes.

- Review DB and DC features that may unintentionally disadvantage women, such as eligibility rules for part-time or temporary workers, treatment of unpaid or partially paid leaves, contribution formulas, vesting or waiting periods, and access to lifetime income options.

- Consider whether adjustments to plan features, over time, might better support continuous and adequate savings across different career paths.

- For DC plans in particular, lower contributions and more conservative investment choices can compound over time, while in DB plans, service and earnings-based formulas can magnify the impact of career interruptions and part-time work.

- One example of this in practice is the shift that many DC plan sponsors have made from target‑risk funds to target‑date funds as the default, so that asset mixes are aligned with members’ expected retirement dates rather than self‑selected risk profiles. Changes like this can help members who might otherwise choose conservative options, including many women5, stay on a more appropriate long‑term investment path.

5. Implement targeted communication and nudges

Retirement outcomes, even of well‑designed plans, depend on informed decisions from members. Targeted communication and behavioural nudges can help ensure that the features intended to narrow gaps are understood and used effectively.

- Tailor financial education, prompts and decision-support tools for segments at higher risk of under-saving, including those with more frequent career breaks or transitions between full-time and part-time work.

- Use key life moments (hiring, promotion, parental leave, return to work, pre-retirement) as opportunities for timely, supportive communication.

Taken together, these actions can help organizations build a clearer picture of their own gender pension dynamics and identify where relatively small changes might have a meaningful impact over time.

Using Today’s Momentum to Shape Tomorrow’s Outcomes

Closing the gender pension gap begins with awareness and the data that sits behind it. For boards, pension committees and total rewards leaders, an important early step is simply to bring the topic into existing conversations about pay equity, representation and workforce planning and sustainability, and to recognize that retirement outcomes are a natural part of that dialogue.

Applying a total rewards lens can help employers look across pay, benefits, retirement programs and career pathways to see how these elements work together or, in some cases, may unintentionally amplify existing gaps. Emerging pay transparency and pay equity initiatives across Canada offer a useful catalyst. As organizations review “who gets paid what today,” many may also choose to extend that lens to “who retires with what tomorrow,” at a pace that reflects their strategy, resources and culture.

By gradually embedding gender-aware analytics, thoughtful plan design reviews and clear lines of accountability into governance, plan sponsors can move from curiosity and diagnosis toward shaping retirement outcomes that are more closely aligned with their values and long-term business objectives.

Lilach Frenkel

Partner, Wealth Solutions, Aon

Lilach is a Partner at Aon and a seasoned actuary with over 25 years of experience in the pension industry working with various stakeholders to manage and meet risk objectives through strategy and innovation. Lilach provides strategic advice to plan sponsors, boards and pension committees on initiatives related to plan design, policy reform, funding and accounting for pension plans.

Previously, Lilach was a Director of Product Innovation at a public sector pension plan where she developed products and initiatives opening new strategic opportunities and risk mitigation techniques for the plan.

She often speaks and writes about plan sponsor risk management and decumulation strategies as well as member engagement as a means to drive best outcomes.

Lilach has volunteered on numerous committees of the Canadian Institute of Actuaries, the Society of Actuaries and the Financial Services Regulatory Authority of Ontario. Lilach is a Fellow of the Canadian Institute of Actuaries (FCIA) and a Fellow of the Society of Actuaries (FSA). She holds a degree in Actuarial Sciences from the University of Toronto.