Articles of Interest

Real Estate as an Inflation Hedge and its role in Pension Plans

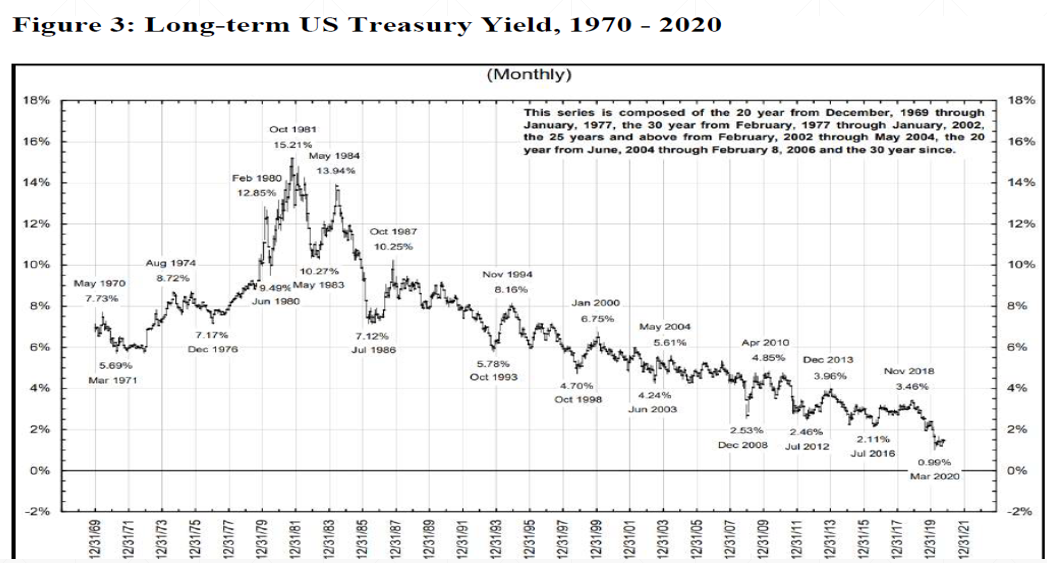

Since the peak in interest rates across the entire yield curve in the early 1980s, bonds had been an integral part of pension portfolios, they provided income for retirees, capital appreciation and diversification benefits as investors saw rates go from 20%+ in 1980 to sub 1% in 2020.

Source: https://fred.stlouisfed.org/series/DGS10

This investment environment gave rise to the “balanced” portfolio approach, where Portfolio Managers would use a blend of stocks and bonds providing a hedge against each other. This worked well for over 30 years as inflation declined, growth slowed, and rates dropped. However, the strategy hit a major roadblock in 2009 when short-term rates hit zero, and even went negative in some parts of the developed world.

Source: MacNicol & Associates Asset Management Inc.

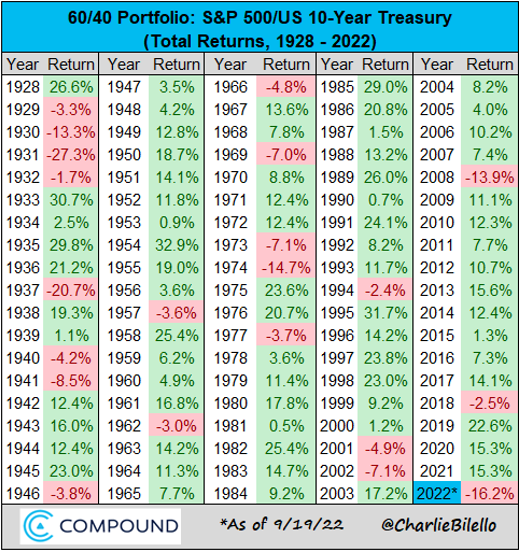

Currently, our view on bonds is somewhat pessimistic given a hawkish Federal Reserve that is expected to hike rates 125bp by year end and another 25bp in 2023. Moreover, inflationary pressures are proving to be stickier and broader than what the market was expecting, and inflationary risks are much higher than during the past three decades, protectionism, deglobalization, underinvestment in the commodity sector and climate change policies pose risks not seen in the recent past. Therefore, in our view, the likelihood of a pension portfolio underperforming using a simple “balanced” approach is high. We can see this by the underperformance of the 60/40 portfolio as of Q3 2022.

Source: Compound Advisors: https://compoundadvisors.com/2022/10-chart-thursday-9-15-22

So what can be done under this investment environment?

Well, it isn’t all doom and gloom. We believe that adding Alternative Asset investments, including real estate to a traditional investment strategy can complement existing portfolios and add another layer of diversification, all while simultaneously increasing expected returns. Real estate is considered a hybrid investment because it has both, bond, and stock like characteristics. Lease agreements bind tenants to make, regular, periodic payments but exposes the investor to the credit risk of the tenant. Additionally, uncertainty at the end of the lease period, around the tenant renewing the lease or needing to find a new tenant, and the ambiguity about the new rental rate at which the lease rate will reset, exposes the investor to equity risk.

Source: CFA Institute

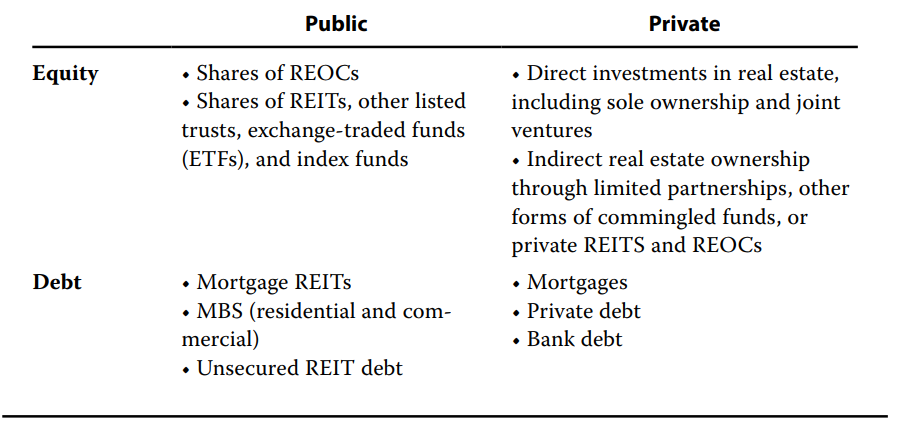

However, not all real estate is equal. Certain types of real estate provide better diversification benefits and better inflation protection than others. The first differentiating factor is between public vs. private real estate. Public real estate investments are usually structured as Trusts, and these investments trade in an exchange with prices fluctuating daily behaving much like regular stocks would. Their market value can trade at a premium or discount to its Net Asset Value (NAV) depending on market conditions. These types of investments are more correlated to equities and have higher “perceived” volatility because price discovery happens daily and can at times trade on emotion and market sentiment.

On the other hand, private real estate investments are commonly pooled investments that allow high-net-worth individuals and institutional investors to get exposure to real estate assets. These assets do not trade on an exchange, their NAV is calculated quarterly or monthly, and units are bought or redeemed at NAV. These types of real estate investments offer better protection against inflation, and subsequently lower volatility, because they are less correlated to the equity market. Furthermore, prices are derived from observable market inputs such as cap rates, net operating income (NOI) and growth rates, which in turn are derived from inflation, real GDP growth, risk premiums and cashflows.

Real estate investments can further be divided into equity and debt investments. Equity investments include office buildings, industrial properties, residential properties, and land. Debt investments come in the form of mortgages where investors lend capital and receive interest in return. Debt real estate investments act like bonds, and do not provide much protection against unexpected inflation. However, equity investments do provide significant protection, especially residential real estate.

Source: CFA Institute

To understand how real estate can offer protection against inflation one needs to understand how properties are valued. There are two basic ways of valuing a real estate asset.

Replacement cost

Replacement cost refers to the cost to replace or build the existing asset from scratch. In this process, investors incorporate the cost of land, permits, raw material, labour and even developer profit. We always want to invest in properties that are sold below replacement cost. This provides a margin of safety when making an investment, as it decreases the probability of a competing asset being built close and competing with our older asset. All things being equal, inflation will increase the replacement cost of a property.

Cap Rate Method:

The basic formula to value a property using cap rates is:

Value of the property = Net Operating Income ÷ Capitalization Rate

Where:

Net Operating Income (NOI) is the expected annual revenue generated by the property minus all the expenses incurred by managing the property, and the capitalization rate is derived by deducting the growth rate (rent Inflation) from the discount rate (risk free rate + risk premium). Thus, if projected 1-year NOI today is $6, and the cap rate is 6% (8% discount rate and 2% rent Inflation) the formula reads $6/6% = $100.00, making the value of the property $100.00. As NOI increases, or cap rates compress, property values will increase and vice versa.

Following the example above, imagine we buy the property for $100.00. Capitalization rates stay at 6% and inflation expectations are 2%. The discount rate is 8%, you use no leverage, you pay no taxes, and we assume rents increase at the rate of inflation. Next period, you will cashflow $6 or 6%, and your property value would appreciate by 2% since the new property value will be $102 ($6.12/6%=$102.00) where the new NOI is derived as $6*(1+2%) = $6.12. Therefore, your total return would be 8%. Now all else equal, if inflation expectations increase to 4% and the same assumptions hold, your total return would be 10%, broken down as 6% cashflow plus 4% capital appreciation.

In this example, we can see that if NOI growth keeps up with inflation and interest rates and risk premiums stay constant or increase at a lesser rate than inflation, real estate will provide inflation protection. However, usually as inflation increases, interest rates and credit spreads tend to increase, putting upward pressure on cap rates. Additionally, it is likely maintenance expenses will increase, putting downward pressure on NOI. Therefore, a buy and hold strategy without repositioning the property, and using no leverage, will only work as a hedge if interest rates or spreads are rising at a lesser rate than inflation expectations, and revenues increase at the same or faster rate than maintenance expenses.

Since real estate is a levered strategy, let’s use another example. We buy the same property for $100 but use a locked in 2% interest only fixed rate mortgage to borrow 50% of the funds to purchase the property. Inflation is 2% and cap rate is 6%, the same as the other example. In Year 1, your interest payment will be $50*2% = $1. Your total return in Year 1 will be $6 cashflow + $2 capital appreciation - $1 in interest, making your total return $7, and your return on investment (ROI) coming in at $7/$50 = 14%. Now let’s assume that inflation shoots up to the current 8%, and you locked this mortgage in at 2%, which was the 5-year fixed mortgage rate at the beginning of 2021. Then your return would equal ($6+$8-$1) = $13, and your ROI would be ($13/$50) = 26%. Of course, this is a major oversimplification of the process. However, as a general rule of thumb, if one can get fixed mortgages below the realized rate of inflation, inflation will boost returns.

From the example above one can conclude that real estate assets work as an inflation hedge if:

- Rents grow faster than maintenance cost, as the property is repositioned, and value is added by the manager (unnecessary expenses are cut, renovations may be made, and market gaps are closed).

- Rents match or exceed inflation.

- Rent inflation (NOI Growth) exceed increases in the discount rate (Risk free rate + Risk Premiums), creating an environment of decreasing real yields.

- Long term debt is fixed and low, devaluing the real cost of debt.

- High tenant turnover rates so rents reset at higher market rates.

Real estate performance vs. the broader market

Understanding how properties are valued can help you understand how real estate can theoretically provide inflation protection under certain conditions. However, it is important to consider how real estate has performed empirically during inflationary periods. To do so we will use a 2011 Wharton study where researchers analysed whether US public REITs provided inflation protection from 1 to 12-month periods of high inflation, with the base case being a period of 6-months. They defined high inflation as periods where CPI was higher than 3.2%, and the data used was from January 1978 to August 2011. There were 199 months of high inflation in the sample, and the results are listed in the table below:

Source: The Wharton School of the University of Pennsylvania – p. 7 https://realestate.wharton.upenn.edu/wp-content/uploads/2017/03/716.pdf

Success rate was defined as total returns that matched or exceeded inflation. As one can see the two assets that provide the most inflation protection are commodities and real estate. It is important to note that the inflationary pressures of the 1970s where mostly commodity driven. Thus, it makes sense that commodities where the best performers.

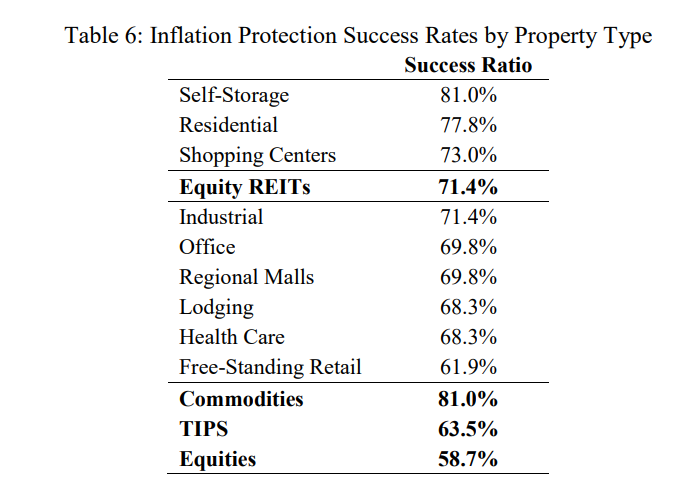

They also analysed different types of real estate to see which type provided better inflation protection. The results can be found in the chart below:

Source: The Wharton School of the University of Pennsylvania – p. 16 https://realestate.wharton.upenn.edu/wp-content/uploads/2017/03/716.pdf

Not surprisingly, the study found that property types with the shortest lease terms and higher turnover had higher success rates as rents were able to reset at higher rates. Whereas properties that had longer lease terms had lower success rates

Finally, it is important to note that like any other asset class, investing in real estate comes with risks. The most important ones to consider are:

- Demand and Supply Risks: Real estate is cyclical with cycles lasting 20 years on average, the sector is characterized by periods of over and under investment with boom-and-bust cycles.

- Valuation Risks: Low availability of capital, lack of information such as lack of comparables, lack of liquidity and a rising interest rate environment can negatively affect the value of a real estate asset.

- Operational Risk: Real estate comes with operational risks related to management, lease provisions, obsolesce, leverage and environmental risks.

In our view, real estate is an asset class that will keep playing an integral role in traditional pension portfolios since it can provide income, growth, diversification benefits as well as inflation protection in a world where stable yield and growth is hard to get while inflationary risks are at its highest levels in 20 years. Of course, this is not the only asset class that should be added to a pension portfolio, other alternative assets such as commodities, private equity and specialized hedge fund managers should be considered, and we have been adding a mix of these assets to our client portfolios since 2009. However, we believe in the current environment real estate assets offer good risk-adjusted returns relative to other traditional assets and their unique characteristics make the asset class an excellent addition to a pension portfolio.

Cesar is registered as Associate Portfolio Manager at MacNicol & Associates Asset Management Inc. where he specializes in the commodity and alternative asset sector. Additionally, he is responsible for client relationships and business development. He holds a bachelor's degree in Financial Business Economics from York University and he is a CFA charterholder.