Articles of Interest

Navigating Decumulation Challenges and the Role of Retirement Literacy – Part 2

Canada’s working population has never been older, with more than 20% of working-age Canadians being close to retirement.1 This, combined with increasing lifespans means a large number of Canadians will be spending the next 30 plus years in retirement. Such statistics are in the part the reason we need to focus on decumulation strategies for Canadians and help overcome challenges throughout the decumulation journey.

Part 1 of the Navigating Decumulation Challenges2 series discusses the importance for Canadians retiring today to consider numerous trends and themes while planning for retirement. Understanding various retirement spending patterns, the impact fees have on retirement income and increasing longevity are examples of such principal factors. In this article, we will continue to examine some of the key considerations that can help overcome such challenges such as retirement replacement ratios, and diversified retirement income portfolios. We will look at the role that retirement literacy and modeling play in retirement planning and in mitigating decumulation risks and obstacles.

Retirement Replacement Ratios

In order to create a robust retirement plan, it is important to understand how much annual income Canadians will need. We often think about this income in terms of a replacement ratio - the percentage of annual income earned prior to retirement that a retiree will need to live comfortably. A long-standing rule of thumb has been to target a 70% replacement ratio.3 The rationale behind this, is that certain expenses cease upon retirement. These include: savings/contributions toward retirement, work-related costs like transportation and lunches, and other potential expenses related to children that may decrease around the same stage of life. That said, other expenses could arise in retirement, like health premiums that may have been covered by an employer prior to retirement. Furthermore, in the first few years of retirement many retirees often increase travel and entertainment spending. In fact, the replacement ratio is highly dependent on various individual factors such as:

- home ownership/property rental

- family composition – single/married with/without (dependent) children

- urban/rural living

- workplace pension and the type of retirement income (DB/DC); and

- debt at/close to retirement

Analysis surrounding these variables suggests that the replacement ratio can range anywhere from 70% to 95%. The replacement ratio depends, among other things, on income prior to retirement, what percentage of it is covered by government benefits such as CPP and OAS, whether you have access to a workplace pension and the type of workplace pension plan you have.

Retirement literacy helps highlight the key circumstances that may shift target replacement ratios. An analysis of the level of income at retirement and simple, easy to understand information about the necessary inputs to estimate that income are essential. Accessing a modeler is a great first step in helping retirees understand the specific replacement ratio they should target in relation to the considerations listed above. Modeling will simulate and drive home the financial impact the above factors may have on retirement income.

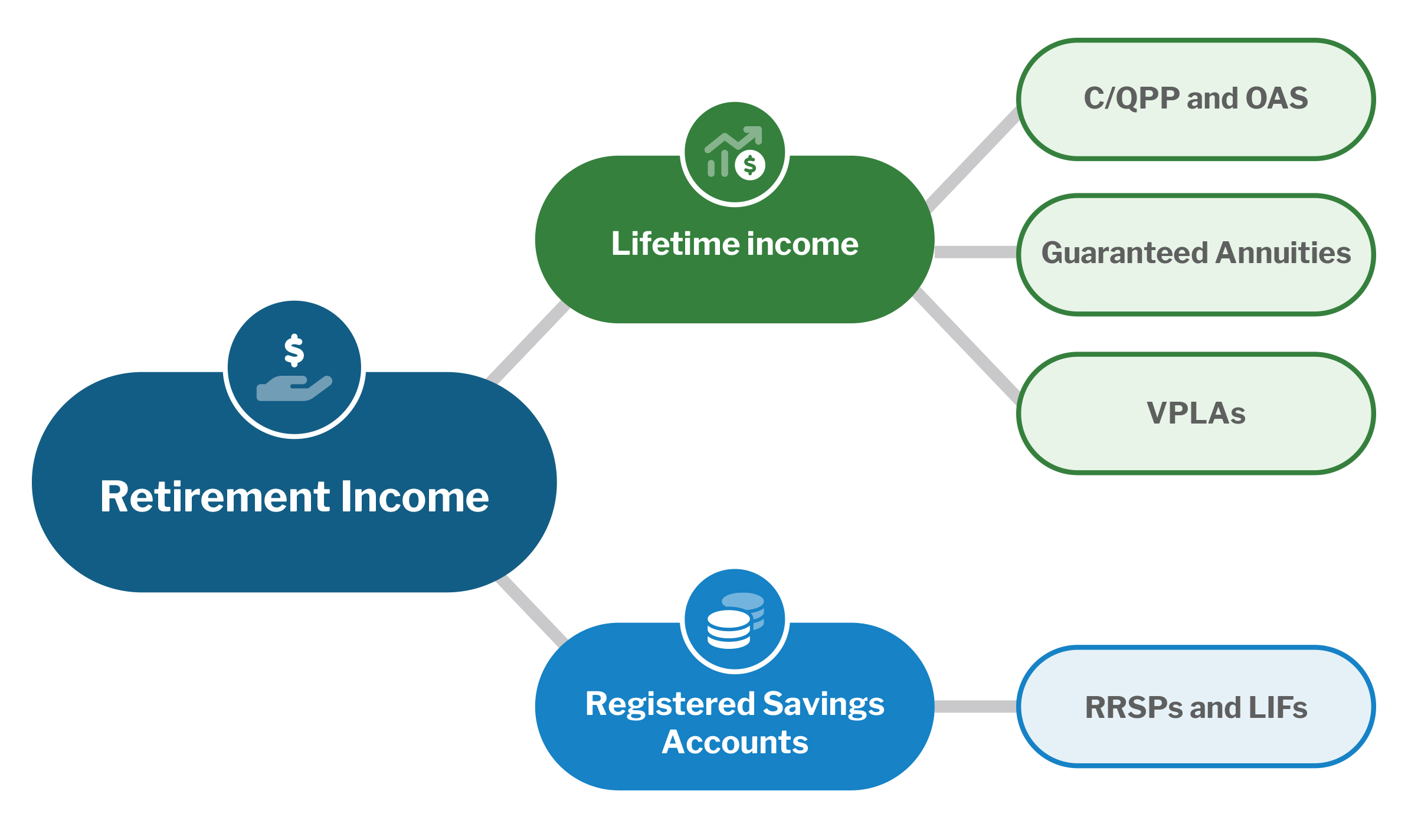

A diverse retirement income portfolio

Once a target retirement income has been established, it is important to consider the multiple sources of income available and combine them in a way that is optimal in order to achieve the desired standard of living and mitigate key risks. Typically, retirement income sources can be divided into two categories4:

- monthly payments payable for life, and

- lump sums (registered savings accounts) that are drawn down periodically.

We can further breakdown the lifetime income category into a variety of options:

- government benefits,

- guaranteed annuities (for example payments from an employer DB plan), and

- variable annuities (such as Variable Payment Life Annuities (VPLAs)).

All sources of lifetime income provide longevity protection since payments will continue as long as the retiree is living. However, each of these sources of lifetime income play a different role within a holistic, diverse portfolio.

Government benefits increase with inflation annually but are not intended to replace all pre-retirement income.

Guaranteed annuities provide a stable, monthly income but usually do not increase with inflation, and their purchasing power therefore often erodes over time.

Variable Payment Life Annuities (VPLAs) are an innovative and cost-efficient solution to converting lump sums into lifetime income. Unlike guaranteed annuities, with VPLAs retirees can participate in market returns. This means, VPLA payments will increase during periods of favourable investment returns, although, as the name suggests, may also decrease as a result of unfavourable market returns.

Registered savings accounts are another source of income at retirement. Such accounts provide exposure to market returns and can provide additional liquidity when needed. However, because such accounts can be completely depleted, there is a risk that retirees outlive these assets.

Each of these various sources of income at retirement meet certain needs/desires and mitigate certain decumulation risks and challenges. For an optimal construction of a diverse portfolio, it is crucial to include all these sources. They each help alleviate different challenges, for example:

- Retirement spending patterns are often not level at various stages of retirementii and having access to additional funds can help accommodate such spending

- Certain sources of retirement income provide exposure to market returns which can yield further income and help protect against inflation in years of strong returns

Combining these options, including those with exposure to market returns, and sources of guaranteed income, can allow a retiree to take on a measured amount of risk, and benefit from the rewards.

Striking the optimal balance to create a diversified retirement income portfolio is key to meeting retirees’ individual needs during retirement. It is by incorporating various sources of income that retirees can mitigate many of the decumulation challenges they are faced with throughout retirement.

Retirement literacy and modeling of the combination of these various sources of income can help Canadians envision the various income streams that can be created at retirement, the needs each stream meets and how to best prepare for the various risks and challenges during retirement.

Mitigating decumulation challenges

Retirement literacy that is comprehensive and easy to understand will help equip Canadians with an understanding of decumulation challenges during retirement as well as solutions to be explored. Modeling is a key part of such retirement literacy. We know that one size does not fit all and that solutions to the various decumulation challenges are often based on individual situations, priorities and desires. Unbiased tools that allow Canadians to create different scenarios, combinations and outcomes will highlight differing needs and help retirees shape best outcomes during their retirement.

2 ACPM | ACARR - Navigating Decumulation Challenges and the Role of Retirement Literacy

4 For the purpose of this analysis, we have not included more complex sources of income such as part-time work, rental income, inheritance, etc.

Lilach Frenkel, Director, Product Innovation, CAAT Pension Plan

Lilach jointed the CAAT Pension Plan in 2022 as part of the Strategic Risk Management team bringing over 20 years of experience in the pension industry. Lilach focuses on the development of partnerships, products and initiatives which provide strategic opportunities and risk mitigation to the Plan.

Prior to joining CAAT, Lilach was a Partner at AON, providing strategic advice to plan sponsors, boards and pension committees on plan design, pension reform, funding and accounting for pension plans.

Lilach has volunteered on numerous committees of the Canadian Institute of Actuaries and the Financial Services Regulatory Authority of Ontario. Lilach is a Fellow of the Canadian Institute of Actuaries (FCIA) and a Fellow of the Society of Actuaries (FSA) and holds a degree in Actuarial Sciences from the University of Toronto.