Articles of Interest

Candid Confessions: Young and Mid-Life Adults Speak Out on Financial Realities

Introduction

In a world where financial independence is a sought-after goal, understanding retirement savings and planning is not just a choice, it's a necessity. Yet, for many, the road to financial security is riddled with complexities and uncertainties.

ACPM spoke with five individuals at various stages of their careers and lives to get a candid look into their financial awareness, challenges, and strategies when it comes to retirement planning.

Their stories are not just personal narratives; they reflect a broader societal need for accessible financial education that resonates with the unique circumstances of each individual. Their journeys underscore the importance of demystifying retirement savings and planning, empowering each individual to take control of their financial future.

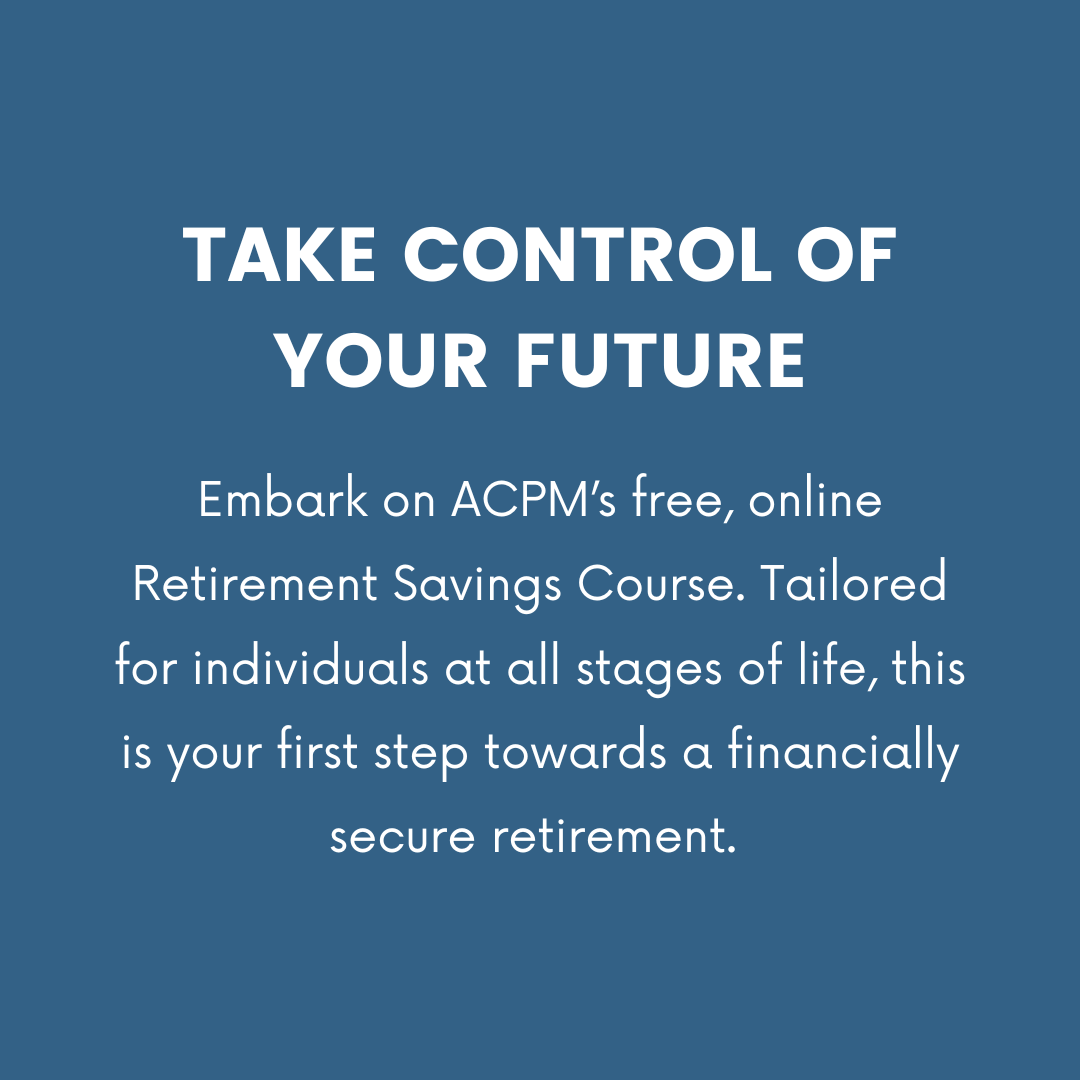

Throughout the article, we offer helpful resources to learn about the importance of financial literacy and developing a retirement savings plan including taking our own free, user-friendly, online Retirement Savings Course.

And now, meet Alessandra, Gwen, Matthew, Olivia and Rachel.

Alessandra, 51, Self-Employed

Alessandra is a graphic designer who's her own boss. Her understanding of retirement savings and planning is, in her words, "very moderate."

“I’m ashamed to say that I haven’t yet started saving for retirement,” she confesses. “I’m aware of its existence and importance, but never took the time to educate myself in depth about options and best strategies,” she says.

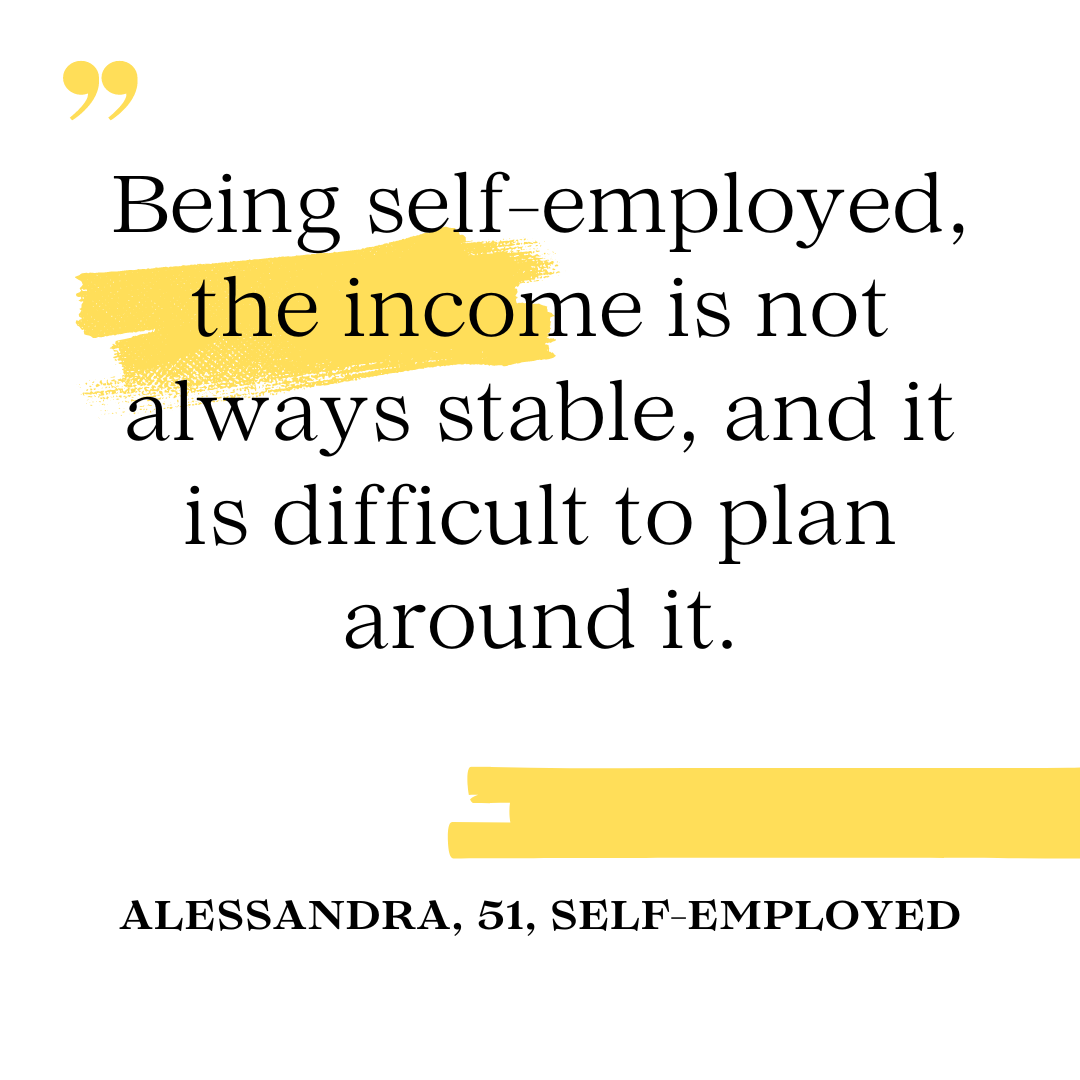

“Being self-employed, the income is not always stable. It’s difficult to plan around it. Life challenges and unexpected expenses always push back the start time,” she adds.

Alessandra has primarily turned to online resources for her information, particularly government websites, which are known for providing reliable and detailed information. However, she says, “I would probably feel more comfortable having a financial advisor helping me to make decisions around investments for my retirement.”

“My generation (and previous ones) were not informed well enough for this crucial life planning need. Younger generations grew up with a greater level of financial education through online resources and most importantly immediate and easy access to saving apps, “she says.

Alessandra revealed she’s increasingly worried about her retirement future since the pandemic. “The pandemic brought up more questions and concerns. I started looking around and trying to educate myself on what can be the best option and approach for my situation,” she says.

She also confided that at the moment she isn’t confident about being able to save enough for a comfortable retirement. “But this might also be because I haven’t planned for it yet and it’s still an unknown factor to me,” she says. On the bright side, she says, “planning can make a big difference to both expectations and experiences of retirement.”

Gwen, 19, Student

Gwen is a student whose frankness is as refreshing as it is enlightening. While she’s familiar with the basics, like pension plans and the principle of saving for the future, she’s the first to admit that her financial literacy doesn’t extend much beyond that.

“I don’t have that good of an understanding of retirement savings and planning – or any financial literacy beyond ‘debt is bad, pay your bills’,” she says. “I – very vaguely – know that pension plans exist and that you pay money to get money down the line. Anything beyond that? Yeah, no, I know about as much as a magic 8-ball,” she quips.

Gwen’s challenge with financial literacy is foundational – the sheer lack of practical financial education leaves her feeling unprepared to navigate the complexities of personal finance such as budgeting, bills, and savings. “I really wish there’d been a class in high school ‘Adulting 101’ that covered stuff like this,” she says.

She believes that everyone should be knowledgeable about these areas before leaving home for university or college. “Seriously, high school is so academically-focused these days that there’s no life-prep – nothing to help us outside of school or in the workplace,” she adds.

Gwen confided that her generation is disillusioned when it comes to economics and finance. “Previous generations have had a sense of hope or ambition when it came to their financial achievements: paying for post-secondary education, buying a house, buying a car,” she says.

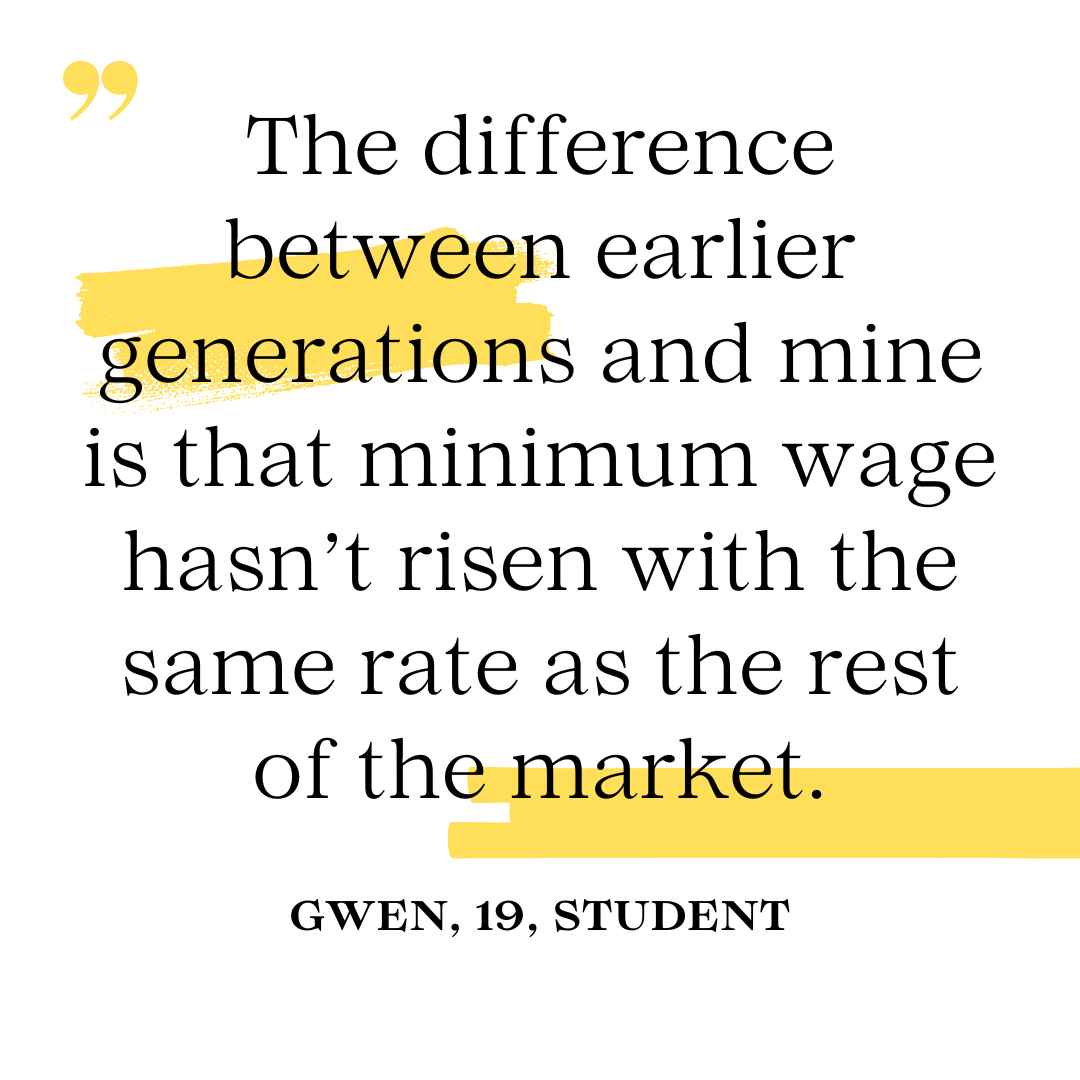

“The difference between earlier generations and mine is that wages, specifically minimum wage, haven’t risen with the same rate as the rest of the market. The goalpost is no longer to buy a house, it’s to rent an apartment without roommates,” she adds.

Although she’s had adults tell her how important it is to save for retirement and how you need to start early, she says, “right now, I’m just trying to save for my education, buying a car, or moving out of my parent’s house.”

Matthew, 41, Business Owner

As an entrepreneur, Matthew is no stranger to the intricacies of running a business. Yet, when the conversation shifts to retirement savings, his confidence wanes.

“I understand the basics of retirement savings and need of it, but the details as well as a lot of the intricacies of what will be needed are still unknown,” he says. “It’s a known unknown and there is an interest in finding out more, but the incentive just hasn’t kicked in yet,” he adds.

Matthew highlights the relentless pressure of maintaining a small business amid soaring living costs. “I’ve tried to keep my head afloat for the last 10 years. Granted it’s doing what I love, but not much financial savings or planning long term has gone into my personal life,” he says. “I’m ashamed to say that I have no RRSP or TFSA that I’m aware of,” he says.

Still, Matthew gives himself a more than 50% confidence rate that he will be able to have enough to live comfortably in retirement, “be it locally, continuing to find innovative ways to make money or through my businesses,” he says. “However, there’s a part of me that knows it’s not 100% guaranteed and I should be seeking that out,” he adds.

“It [retirement savings] has grown ever more in the back of my mind as well as my partner’s,” says Matthew. “We are both aware of the years of saving for it are ticking away, but unfortunately haven’t been able to do much yet. There are five and 10 year long plans we want to achieve that will start it, but it has yet to begin,” he adds.

Matthew reflects on the advantages he believes the previous generation had going for it such as housing that cost less than a down payment is today, and growing areas of industry where long-term job security was a thing rather than a best practice of moving companies every five to 10 years.

He also candidly states that “while it may sound morbid, there’s also a lot more riding on old age pension now that wasn’t an issue for the previous generation since life expectancy has gone up.”

Olivia, 24, Marketing Coordinator

Olivia represents the voice of the younger generation at the beginning of their careers. As a marketing coordinator, she's at the forefront of trends and digital innovation. Yet, when it comes to the future of her finances, she takes a more conservative stance.

“My understanding of retirement savings and planning is very minimal other than the key understanding that it is important to do and to start planning for it from a young age,” she says.

Although Olivia hasn’t formally started saving for her retirement, she says she works hard on ensuring that her finances are in a comfortable position with a gradually increasing amount, no matter if it's big or small. She says it’s important for her to have a safety net should something happen where she’s not making an income for a few months and to be careful with her spending. “I don’t live above my means and have never lived paycheck to paycheck,” she says. “I plan on starting to work on a proper retirement savings plan in the next couple of years by the time I am 30,” she adds.

Olivia also alludes to the cost of living as a challenge she’ll face when she officially starts saving for her retirement. “It can be difficult to put money aside when the cost of expenses such as rent, food, transportation, and other essentials as well as entertainment costs take up a large part of monthly income,” she says.

"Currently, I’m lucky to be living in a place where the rent is lower than the average due to securing it during the COVID pandemic, and to be earning an adequate income,” she says. “However, as the cost of living becomes higher and my general living expenses will likely increase, I have begun being more frugal and intentional with entertainment and non-essential expenses as well as being more cautious with costs related to essentials like food and clothes,” she adds.

While saving for retirement is important to Olivia, she reveals, “I find that especially now when money is tight for a lot of people, it often takes a back seat to other more essential financial priorities.”

Rachel, 31, Lawyer

As a lawyer, Rachel is adept at navigating complex legal landscapes but finds herself in more uncharted territory when it comes to retirement planning. "Let's just say, my knowledge is pretty basic," she says with a laugh. It's a candid admission and one that resonates with many young professionals who find themselves caught up in the immediacy of career demands.

Rachel’s main challenges are student debt and the cost of living. “Paying off my law school debt (Ontario Student Assistance Program and student personal line of credit) is my number one financial priority at the moment,” she says.

“Ideally, if I had the disposable funds, I would invest the most amount of money in a tax-free savings account (TFSA) or an account that would yield the highest earnings, but I would try to manage a diversified portfolio.,” she adds.

Rachel confesses that financial advisors have sought her out as a potential client given her profession, but says, “at this point in my life, I cannot afford to save more than $100 per month. I’ll have to make drastic changes to my lifestyle in order to contribute more to my retirement savings and reach my retirement goals. I also have an empty RRSP account because I currently don’t make enough money to save.”

Yet, despite these hurdles, there's a palpable sense of determination and hope. “With the right information, guidance, and advice, I’ll feel confident in my ability to save for retirement. I recognize that I need to better manage my finances and eventually pay off my student debt,” she says.

“My generation (millennials) have a more relaxed attitude about retirement savings. We are a generation of consumption and instant gratification, and social platforms like Instagram and TikTok fuel the fire,” says Rachel.

Even though, she says, “I plan to retire at the age where I can live a comfortable life. If I must work until I’m 70, then so be it, as long as my job is not strenuous or stress-inducing.”

Stay tuned for more

The perspectives of Alessandra, Gwen, Matthew, Olivia and Rachel underscore the evolving attitudes and challenges each generation faces regarding retirement savings. From the advantages of previous generations to the economic hardships and changing priorities of current ones, it’s clear that retirement planning remains a complex and pressing issue across all age groups, requiring adaptive strategies and awareness to navigate the ever-changing financial landscape.

Stay tuned for other articles on financial literacy where we offer more insights and solutions.

This article is shared in tandem with the FSRA 2024 Pension Awareness Day

ACPM (Association of Canadian Pension Management)